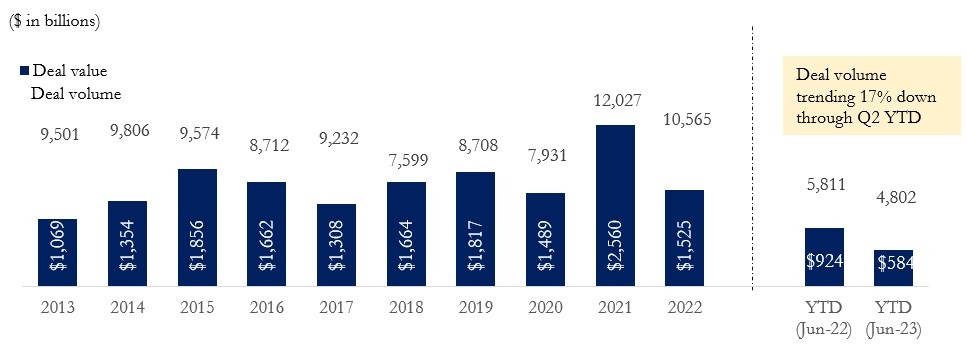

After a less than enthusiastic start to the year (M&A volumes were way down), we are starting to see strong signs of a potential resurgence / rebound in activity. First, let’s look at the data so far this year:

On a year over year basis, actual M&A volume in the US was down meaningfully ~ – 17%. Reasons for the decline primarily stem from rising interest rates and continued concern about macroeconomic conditions with inflation at the top of these concerns. This backdrop has led to buyers pushing back on valuation, clearly demonstrating less confidence about the future growth of either their own business, the target business, or both, while also managing higher cost of capital. This should make a lot of sense – capital is more expensive and the economic outlook is not as sunny.

We have seen the same dynamic at play with the all-important measure of the future health of the M&A market – capital raising activity. We measure capital raising so closely because it gives us a really good indicator of how positive the institutional investors view the current M&A market – specifically whether they are willing to open their checkbooks or not. This also gives us a strong perspective on the amount of capital “sitting on the sidelines”. Let’s look at the data through the first half of the year:

As you can see in this data, institutional capital raising supporting private equity firms have similarly declined. While it makes a lot of sense to see this would happen in light of higher interest rates and macroeconomic concerns, it nevertheless gives us less than positive vibes about the future direction of the M&A market. That said, we are still coming off of a very robust year in 2022 where it seemed like every PE firm on the planet was raising money. So the good news is that, although the year to date capital raised is down 22%, we are still working off several years of unspent capital. So it begs the question, if M&A volumes are down, why would institutional investors allocate more capital to private equity when the general partners who they have backed already have plenty of capital? This makes sense to us.

However, clearly capital is becoming a bit more constrained. And as we proceed through the current environment, sellers would be wise to lower their valuation expectations that reflect this sentiment. Fortunately for sellers, their opportunity to invest the net proceeds from a sale are much more high-yielding instruments than we had just 12 months ago.

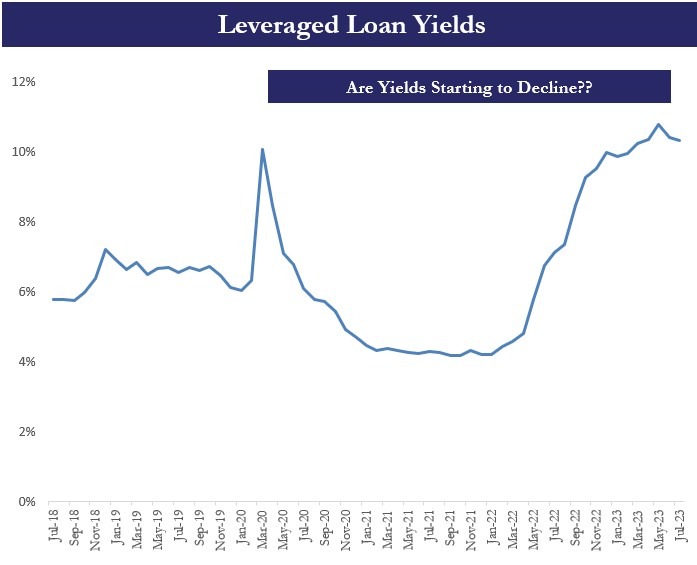

In a positive sign, we are definitely observing a stabilizing loan yield environment. This is great news. As we have said before, volatility is not a tailwind for M&A volumes – stability is, however. Stable yields are a welcome sign; when they start to decline, we expect buyers will come out of the woodworks.