First of all, why the interest in the HVAC-R sector?

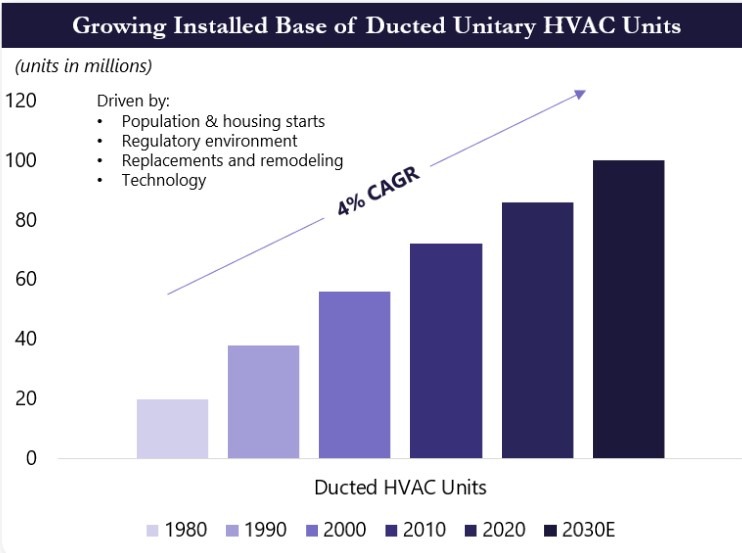

Since the dawn of ducted heating and air-conditioning, the number of HVAC units installed in homes has expanded to the point where almost every single building structure has some heating and / or cooling system inside. Today there are nearly 100 million ducted units inside the 140 million housing structures across the United States (there are still many window units in operation).

These units are not only growing from an installed base standpoint, but they are also getting replaced from age, storm activity, regulatory changes and overall technological improvements.

This is a very healthy backdrop for investment activity. All of these installed units create demand for replacement and maintenance expenditures. And as everyone knows and appreciates, when these units break or need service, they have to be fixed or otherwise maintained. Given the increasing complexity and interconnectedness of these units, this is not a problem that can be fixed even by some of the most capable DIY’ers out there.

The HVAC-R supply chain is massive, complex and increasingly consolidating. The OEM part of the supply chain is highly consolidated with Trane, Carrier, Daikin, Lennox, York and Rheem and their sub brands dominating the unit volume. This is a $25 billion market and growing nicely.

Downstream from the OEM is an increasingly consolidating distribution industry though still remains significantly fragmented. Watsco and Ferguson are the two largest strategic players in this market and together comprise less than 15% of the market. After these two players, the list expands considerably. Recent entrants have included private equity firms such as Genstar, Gryphon and Rotunda Capital, to name a few. The distribution market is estimated to be 2 to 3x larger than the OEM manufacturing market size.